June CPI: It's Time to Cut Interest Rates

- CitizenAnalyst

- Jul 11, 2024

- 5 min read

We got another outstanding inflation report for June this morning. Let's go through it.

Core CPI for the month increased 0.1% month-on-month (and seasonally adjusted), while headline CPI (which includes food and energy prices, which the core does not) actually decreased 0.1%. Rounded to the second decimal place, core CPI increased only 0.05%. This was the best inflation report since last November when the economy felt similarly as it does today: weak. On a year-over-year basis, June's figures put headline CPI at 3%, and core CPI at 3.3%. While these are still well above the Fed's 2% target, "run rate" inflation is meaningfully lower, and I'll argue below that we may even be below the Fed's 2% target already. Regardless, the Fed's language has been consistent over time. They've claimed they're not waiting until inflation is back to 2% to start cutting interest rates: they simply want inflation to be "on the way back down" to 2% to do so. We have reached that point now. If this data isn't good enough for them to even start, nothing will be short of a recession.

Let's now take a look at our three buckets, as we usually do: goods, services excluding shelter (aka "core services" or "super core"), and finally, shelter inflation. Goods inflation for the month fell 0.04% (so goods prices again fell for the month). Excluding automobiles, goods inflation was still only 0.01% (so still basically flat). Anyone who's shopped at all over the last couple months can attest to the fact that prices are much more reasonable again and sales and promotions are very much back. So this month was generally a "status quo" month in this regard. We're back to pre-pandemic levels of inflation in goods (which was basically zero), and this month has been similar to recent months. This is all good.

Core services inflation was the bright spot of this month's inflation report, similar to last month. In June, services ex. shelter once again fell (similar to last month's 1 bps decline), but this month, this was despite a +3 bps contribution from auto insurance, which has been a bugaboo in recent months but which was flat last month. This makes the -4 bps decline in core services contribution that much more impressive (said differently, core services ex. auto insurance was -7 bps, which is the best reading in this category since March and April of 2020). The chart below shows the contribution from core services excluding car insurance to monthly core inflation, both before and after COVID. It's probably unlikely that these declines continue, since core services has been inflationary even before COVID. But the level of core services inflation has clearly slowed down, likely due to a softer labor market (which is a key cost input for services businesses). The Fed has been very focused on this "bucket" in particular, so this is very welcome news.

Let's now finally get to shelter inflation. As readers of this blog know by now, this has been the most stubborn part of the CPI. The reason (at least we think, anyway) why this element of the CPI has lagged what's happening with rent prices in the real economy is because of the methodology for how CPI calculates this component of the index. If you live in an apartment building with 12 units, and one renews each month at a 3% increase after increasing last year at 7%, it would take 12 months for the building in total to reflect 3% inflation. This is generally how the CPI calculates shelter inflation. We've therefore been expecting a lag in the shelter CPI data, but this lag has been longer and more pronounced than we hoped. This month though, the shelter component of CPI contributed only +9 bps to core CPI, the lowest since August of 2021. This is a welcome improvement from the recent levels of +18 bps (which we saw for each of the last 4 months), and even compares favorably to the +11 bps that we saw pre-COVID. It appears that maybe, just maybe, the CPI has finally caught up to market prices for rents in the real economy. This was potentially going to be the last sticking point for the Fed in reducing rates, but now this obstacle appears to be out of the way as well.

Category level inflation again shows the same thing this month: inflation is close to, if not back to, 2%. Using our Category 4 and Category 5 level data (which consists of 55 and 101 goods and services baskets comprising 98% and 77% of the core CPI respectively), average and median category level price increases remain between 0% and 0.2%. June's specific figures were a 0.1% median increase and a 0.19% average increase for Category 4 level data, and a 0% and 0.09% for average and median Category 5 level data. On an annualized basis, this puts us at something close to if not less than 2%.

The below chart shows the above data on a 3 month annualized basis. The lines remain below the bars, but you can see even the bar has now essentially reached 2%. This is why we said earlier that focusing on the year-over-year figures is too backward looking. It incorporates prior months where inflation was higher in the data. If you try and get a better sense of how much inflation is in the economy today, the number is well below the 3-3.3% stated in the year-over-year figures.

Below is my chart showing where I think true inflation is in the economy today. My best guess is somewhere between 1.3 and 2%. Note that the chart below also adjusts for the CPI shelter lag, and incorporates an +11 bps monthly increase for shelter. Given we were actually (finally) below that this month (recall shelter only contributed +9 bps to this month's figures), these numbers could potentially even be too high.

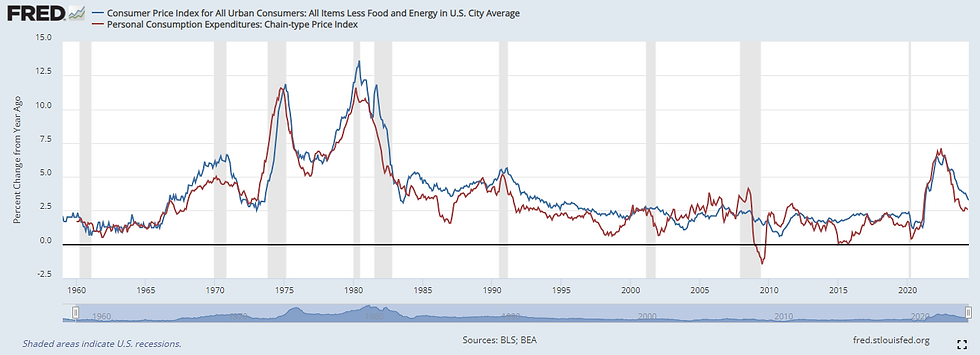

One thing we haven't even discussed that only adds to this case is that the Fed actually doesn't look to CPI inflation levels in its target for 2%: it looks to the Personal Consumption Expenditures Index, which because of its different weightings, historically has been about 30-50 bps below CPI levels. Thus, adjusting our estimates for where "run-rate" CPI is, core PCE may even be closer to 1-1.5% on a run-rate basis. The chart below shows this, with the red line (PCE) consistently being below CPI.

When looked at in the context of the last several months, and also in the context of other economic data in recent months, if June's CPI isn't enough for the Fed to cut interest rates, nothing will be short of a recession. As Chair Powell said to Congress earlier this week, this is no longer an overheated economy. The evidence is now very clear: goods inflation remains flat to negative (indicating prices are decreasing in many cases, not increasing) core services inflation is breaking (likely at least partially due to a weakening labor market), and shelter inflation in the CPI finally seems to be catching up to where it is in the real economy (which is flat to negative). It's time to cut interest rates.

Commentaires